What is an APR?

Your Annual Percentage Rate (APR), as opposed to the interest rate, is a percentage that includes any additional loan costs or fees in it’s calculation. This means the entire finance charge on a loan will be included in the APR calculation. Your APR will be different than your interest rate in most loan scenarios because APR increases when loans include more fees and loan costs.

Overall, an APR will give you a better idea of what your loan will cost you than anything else, including interest rates. This is mostly because it includes other fees that we mentioned above.

Compound or Simple Interest

The amount you are charged for your loan will depend entirely on whether your lender uses compound or simple interest. Simple interest is paid in full when you make your monthly payments in full and on time. You can lower the overall amount of interest you pay on your loan with simple interest by paying your bills in full in advance.

Compound interest is calculated based on existing interest and newly charged interest. Basically, that means you’re paying interest on your interest. A lot of credit card companies charge compound interest, which means you’ll likely end up paying more in your overall APR.

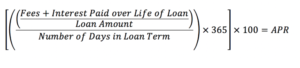

Calculating APR

It’s not very hard to calculate APR. You add your fees to the interest paid over the life of the loan. Then you divide that number by the loan amount. After you’ve calculated that, take the new number (fees+interest paid over life divided by loan amount) and divide it again. This time by the number of days in the loan term.

Multiply the number you get from that calculation by 365. Then multiply once more by 100. That will give you your APR.

For more information on calculating APR, or the loan options that might be available, go to Liftcredit.com. Review the site for more financial terminology and to get in touch with financial and loan experts.